- Þetta er einmitt þ.s. verið er að benda á, þ.e. að stóra gengisfellingin sem margir bölva var í raun og veru jákvæður atburður fyrir þann grunn sem allt stendur á, þ.e. atvinnulífið.

Bloggfærslur mánaðarins, júlí 2010

15.7.2010 | 20:24

Ömurleg staða Orkuveitu Reykjavíkur!

Eins og fram kemur í fréttum í dag, þá er Orkuveita Reykjavíkur í skuldakrísu.

Sjá fréttir:

OR á ekki fyrir skuldum næstu 3 árin

Óhjákvæmilegt að hækka gjaldskrá OR um tugi prósenta fyrr en síðar

Stórkostlegar gjaldskrárhækkanir óhjákvæmilegar hjá OR

- "Orkuveita Reykjavíkur skuldar um 240 milljarða króna, og eru skuldirnar í erlendum gjaldmiðlum að nær öllu leyti."

- "80 prósent af tekjum fyrirtækisins eru hins vegar í krónum."

- "Eigið fé fyrirtækisins hefur brunnið upp frá hruni."

- "Í minnisblaði sem fjármálastjóri borgarinnar kynnti nýlega kemur fram að 20% hækkun gjaldskrár mundi aðeins duga til þess að mæta afborgunum þessa árs."

- "Án gjaldskrárhækkana muni rekstrarafkoman aðeins nægja fyrir greiðslu um 90% af afborgunum og vöxtum þessa árs, 64% af greiðslubyrði næsta árs, 65% af greiðslubyrði ársins 2012 en að Orkuveitan muni aðeins rísa undir 44% af afborgunum og vaxtagreiðslum árið 2013 að óbreyttu."

- "Í tengslum við aðalfund fyrirtækisins þar sem ný stjórn var kjörin kom fram að borgarstjórn ætlaðist til að virkri stóriðjustefnu Orkuveitunnar yrði hætt. Um það hvað þetta feli í sér segir Haraldur Flosi, fulltrúi Besta flokksins: „Það er opinber stefna þeirra sem ég þigg umboð mitt frá að það eigi að hverfa frá áhættusækinni fjárfestingu og snúa sér að öruggri fjárfestingu í þágu almennings."

- "Staðið verði við skuldbindingar sem þegar hefur verið stofnað til en ekki efnt til nýrra fjárfestinga. Um fjórir til sex milljarðar króna hafa farið í að undirbúa nýjar virkjanir á Hellisheiði, þar af um milljarður í Bitruvirkjun, sem blásin var af á síðasta kjörtímabili. Mun meira fé liggur í undirbúningi Hverahlíðarvirkjunar. Orkuveitan hefur átt í viðræðum um að selja orku frá Hverahlíð til kísilmálmsverksmiðju í Þorlákshöfn og til álvers í Helguvík. Þau verkefni, og þar með sala á orku Hverahlíðarvirkjunar, eru í óvissu enn sem komið er. Haraldur Flosi leggur áherslu á að staðið verði við gerðar skuldbindingar gagnvart þessum aðilum en segir að engin önnur áform séu um að Orkuveita Reykjavíkur ráðist í áhættusamar stóriðjufjárfestingar undir stjórn hins nýja meirihluta í borgarstjórn Reykjavíkur."

Sjá upplýsingar úr Fjárhagsáætlun Reykjavíkurborgar 2010. Bls. 114 - 116.

2008 2009 2010

Skuldir. 211.014.534 240.859.954 250.943.959

Handbært fé* -2.507.372 -71.375 -433.021 (tölur yfir lækkun á handbæru fé)

Handbært fé** 3.751.011 1.243.639 1.172.264 (tölur yfir handbært fé í upphafi árs)

Handbært fé 1.243.639 1.172.264 739.243 (Handbært fé í árslok)

- Eins og sést að ofan, er OR stöðugt nú að éta upp sitt lausafé.

- Augljóslega, gengur slíkt ekki nema í skamman tíma.

Niðurstaða

- Ég er ánægður með, að núverandi meirihluti sé að vinna allsherjar úttekt - og, að auki að þeirri áhættusömu fjárfestingarstefnu er fylgt hefur verið um nokkurrt árabil, verði hætt.

- Betra seint en aldrei - en, eftir sytur borgin með sárt ennið. Valkostirnir einungis slæmir.

- Gríðarlegar hækkanir gjaldskrár Orkuveitu Reykjavíkur, á næstu árum.

- Reykjavíkurborg, taki hluta skulda Orkuveitu Reykjavíkur yfir, létti þeim þannig af OR.

Báðir kostirnir skila slæmri niðurstöðu, þ.e. valið er:

- Auknar álögur á almenning, og það stórfelldar. Á meðan getur almenningur í reynd engu á sig bætt.

- Auka skuldir Reykavíkur og þar með vaxtagjöld Borgarsjóðs, sem mun minnka svigrúm borgarinnar til að, standa undir kosningaloforðum um aukningu fjármagns til margra þarfra hluta.

Þessi niðurstaða er mikill áfellisdómur fyrir þá er hafa setið í stjórn Orkuveitu Reykjavíkur umliðin ár, og þeir hafa verið fulltrúar allra hinna hefðbundnu flokka. Stefna þeirra er réðu OR var þannig blessuð af fulltrúum allra sytjandi flokka á síðustu 2. kjörtímabilum.

Það verður að koma í ljós, hvað ný Borgarstj. gerir á endanum í málinu, þ.e. A)Stórfelldar álögur á almenning eða B)Gefa upp á bátinn kostnaðarsöm kosningaloforð er stuðla áttu að minnkuðu atvinnuleysi í borginni og ímsum öðrum jákvæðum en kostnaðarsömum breitingum.

Kv.

9.7.2010 | 00:37

Hversu slæmt væri, ef Ísland færi í greiðsluþrot? Spurning sem vaknar aftur, þegar á ný er útlit fyrir hrun bankakerfisins!

Það ganga margir mjög langt í fullyrðingum -

- Hér verði Kúpa norðursins.

- Ísland yrði lokað af frá alþjóðamörkuðum fyrir fullt og allt.

- Hér yrði fátækranýlenda.

- Fyrirtækin flyttust burt.

- Það allra versta sem geti komið fyrir.

- Þjóðir heims myndu snúa við okkur baki.

Á VOXEU er að finna áhugaverða grein, sem fjallar einmitt um þá spurningu, hverjar eru afleiðingar greiðsluþrots.

The costs of sovereign default: Theory and reality

Eduardo Borensztein Ugo Panizza

Aðalgreinina þeirra, en greinin í VOXEU er stutt samantekt, sjá (Áhugasamir lesi sig í gegnum löngu greinina):

The Costs of Sovereign Default, Eduardo Borensztein and Ugo Panizza

Eins og þeir útskýra, þá er almennt séð ekki hægt að ganga að eignum ríkja eins og ef um fyrirtæki eða einstakling væri að ræða. Þetta sé vegna prinsippsins " sovereign immunity " þ.e. sem gjarnan er þítt sem "griðhelgi".

Sovereign debt is different. Private debt contracts can be enforced in court and court rulings enforced by asset seizures. By contrast, public-debt creditors:

- Lack procedures for enforcing sovereign debt contracts – partly due to the principle of sovereign immunity.

- Have ill-defined claims on the sovereign's assets as they cannot attach assets located within the sovereign’s borders, and typically have limited success in going after sovereign assets located abroad.

Þetta væntanlega skýrir fyrir einhverjum þeim er ekki vissi, af hverju ákvæðið "Waiver of sovereign immunity" í Icesave samningnum, var svo alvarlegt.

Icesave samningurinn, er hefðbundinn viðskiptasamningur. Er það gott?

Samingurinn við upphaflegur texti: Holland

Samningurinn við upphaflegur texti: Bretland

17.3 Waiver of sovereign immunity

Each of the Guarantee Fund and lceland consents generally to the issue of any

process in connection with any Dispute and to the giving of any type of relief or

remedy against it, including the making, enforcement or execution against any of its

property or assets (regardless of its or their use or intended use) of any order or

judgment. lf either the Guarantee Fund or lceland or any of their respective property or assets is or are entitled in any jurisdiction to any immunity from service of process or of other documents relating to any Dispute, or to any immunity from jurisdiction, suit, judgment, execution, attachment (whether before judgment, in aid of execution or otherwise) or other legal process, this is irrevocably waived to the fullest extent permitted by the law of that jurisdiction. Each of the Guarantee Fund and lceland also irrevocably agree not to claim any such immunity for themselves or their respective property or assets.

En þar var þeirri vörn sem fylgir sjálfstæðinu, varpað af eignum í eigu ríkisins - sem hefði algerlega umturnað hinni þjóðréttarlegu stöðu Íslands gagnvart Bretum og Hollendingum, þ.e. skv. því ákvæði gátu Hollendingar og Bretar raunverulega gengið að eignum íslenska ríkisins, alveg eins og ef Ísland væri fyrirtæki eða einstaklingur, er hægt væri að gera upp.

Munum, að Icesave samningurinn var á einkarréttar grunni, og þannig raunverulega komið fram við Ísland, eins og það væri fyrirtæki eða einstaklingur, með cirka sömu réttarstöðu - þ.e. ekki á grundvelli þjóðarréttar, þ.s. réttarstaðan er allt, allt önnur.

- Ef, Icesave samningurinn hefði gengið fram, hefði raunverulega verið alltof - alltof, hættulegt fyrir Ísland að fara í þrot.

- En, þ.s. honum var í reynd hafnað, gilda enn hin hefðbundnu ákvæði hins alþjóðlega þjóðréttar, þ.e. eignir ísl. ríkisins eru griðhelgar þ.e. hafa " sovereign immunity "

Þ.e. einmitt griðhelgin, sem gerir greiðsluþrot að leið sem er raunverulega fær, fyrir fullvalda ríki.

- Þ.e. þjóðir hætta að borga af skuldum.

- Á móti, hrynur lánstraust alveg - hið minnsta um tíma.

- Allur innflutningur þarf að fara fram á grunni staðgreiðsluviðskipta.

- En hversu lengi stendur þetta ástand, öllu að jafnaði.

- Hve alvarlegar eru efnahagslegar afleiðingar greiðsluþrots?

- Verður viðkomandi ríkjum aldrei fyrirgefið?

Skemmtilegt að skoða graf á bls. 28 ( The Costs of Sovereign Default, Eduardo Borensztein and Ugo Panizza ) þ.s. kemur fram yfirlit yfir fj. ríkja eftir heimsálfum sem hafa lent í greiðsluþroti frá 1824 - 2004. Allar töflur birtar aftast.

Skoðum hvaða svör Borenstein og Panizza gefa.

"We start with reputational costs and show that defaulting countries do indeed suffer in terms of access to the international capital markets. Default episodes are associated with an immediate drop of credit rating and a jump in sovereign spreads of approximately 400 basis points. However, this effect tends to be short lived and disappears between three and five years after the default episode."

- Með öðrum orðum, svokallað skulda-álag hækkar um 400 punkta að meðaltali, þ.e. CDS (credit default swap).

- Að meðaltali, standa neikvæð áhrif yfir á milli 3 - 5 ár.

- En hafandi í huga kreppuna í 3. heiminum á 8. áratugnum, þá var meðaltími ögn lengri, þ.e. 9 ár.

When we look at trade costs, we add support to Rose's (2005) result that default episodes are associated with a drop in bilateral trade, but we are not able to identify the channel through which default has an effect on trade. In a companion paper (Borensztein and Panizza forthcoming), we also find a trade effect using industry-level data but, again, we find that the effect tends to be short lived and only lasts two to three years.

- Þeir finna að viðskipti skaðast í tengslum við greiðsluþrots viðburði, en meðal tímabil neikvæðra áhrifa á viðskipti, séu aðeins 2-3 ár.

When we explore the effect of default on GDP growth, we find that, on average, default episodes are associated with a decrease in output growth of 2.5 percentage points in the year of the default episode. However, we find no significant growth effect in the years that follow the default episode. In fact, quarterly data indicate that output contractions tend to precede defaults and that output starts growing after the quarter in which the default took place (Levy et al. forthcoming). This suggests that the negative effects of a default on output are likely to be driven by the anticipation of default.

- Meðal-lækkun hagvaxtar sem hlutfalls landsframleiðslu í tengslum við greiðsluþrots viðburði, skv. þeirra útreikningum er einungis 2,5%.

- Þeir verða ekki varir við nein merki umtalsverðra neikvæðra áhrifa á hagvöxt, árin á eftir greiðsluþroti.

- Neikvæð áhrif komi fram, skv. greiningu á gögnum, rétt fyrir greiðsluþrot þ.e. að orsök falls í hagvexti sé ekki greiðslufallið sjálft heldur sé hana að finna öllu jafnaði í þeirri röð atburða sem kemur á undan greiðslufalli.

Niðurstaða

Ég er ekki að hvetja til þess, að leið greiðsluþrots verði farin. Á hinn bóginn, virðist ljóst að flest þ.s. haldið er á lofti af þeim, er mála mjög dökka mynd af líklegum afleiðingum greiðsluþrots, sé þvættingur.

- Ábendingin er sú, að greiðsluþrot er raunverulegur valkostur.

- Við eigum ekki að vera logandi hrædd við þá hugsanlegu útkomu.

- Að mörgu leiti, erum við betur í stakk búin að feta þá leið en mörg önnur lönd, þ.s. Ísland býr yfir traustum tekjuleiðum sem ólíklegt er að muni raskast.

- Við eigum einfaldlega að íhuga stöðuna, verandi í andlegu jafnvægi.

- Það að við höfum þetta sem raunhæfa varaleið, á að styrkja stöðu okkar í samningaviðræðum við erlendar bankastofnanir, og já - Breta og Hollendinga.

Ég met stöðuna þannig, að enn sé mögulegt að komast hjá þessu. Einnig, að betra sé að komast hjá þessu, - en á hinn bóginn mega ekki tilraunir til þess kosta of mikið. Ef kalt mat er að, hagstæðara sé að neita að borga, eigum við að feta þá vegferð óhrædd.

Það mun hafa nokkrar óþægilega afleiðingar - ekki má heldur gleima að það má vera, að Íslandi vegni ver en meðaltölur að ofan, gefa til kinna. En, samt værum við ekki að tala um neitt sambærilegt við þær dökku myndir sem ímsir virðast hafa gaman af, að draga upp.

- En, því má ekki gleima að skuldirnar hlaupa ekki frá okkur þó við neitum að borga þær -

- Á hinn bóginn, verða eigendur skulda yfirleitt samningsþíðari eftir nokkurn tíma.

- Á endanum, ef menn vilja aftur öðlast lánstraust þarf að ná samningum við kröfuhafa. En, það má alveg taka einhvern tíma.

Ps. fer nú í sumarfrí í viku. Sjáumst eftir viku.

Kv.

Stjórnmál og samfélag | Breytt s.d. kl. 11:08 | Slóð | Facebook | Athugasemdir (2)

Stjórnmál og samfélag | Breytt s.d. kl. 11:08 | Slóð | Facebook | Athugasemdir (2)

7.7.2010 | 15:49

Bankarnir með svipaðann innlendan starfsmannafjölda og þegar bóluhagkerfið var í hámarki árið 2007

Bankasýsla Ríkisins hefur gefið út mjög áhugaverða skýrslu um starfsemi bankanna. Nokkur atriði vegkja einkum athygli.

Arion Banki Íslands Banki NBIHagnaður eigin fjár 16,7% 35,3% 10%

Ef maður íhugar þetta í samhengi við eldri upplýsingar um hlutfall eiginfjár frá Seðlabanka Ríkisins:

Eiginfjárhlutfall viðskiptabankanna skv. Seðlabanka Íslands.Arion Banki - 13,7%

Íslandsbanki - 19,7%

NBI - 15%

MP banki 15,1%

Samtals 15,9%´

Þá virðist það klárt, að Íslands Banki sé fjárhagslega besti bankinn.

Þá væri ef til vill réttast, að sameina bankana með þeim hætti, að Íslands Banki taki yfir NBI og Arion Banka, eða þá að þeir 2 bankar fari í þrot og síðan Íslands Banki taki yfir þeirra eignir.

Skýrsla Bankasýslu Ríkisins "Ytra umhverfi fjármálafyrirtækja hefur tekið miklum stakkaskiptum frá bankahruni en lengri tíma tekur að breyta innviðum. Þrátt fyrir bankahrunið er hlutfall starfsmanna í fjármálaþjónustu sem hlutfall af heildarvinnuafli svipað og það var árið 2007 er stefnt var að því að gera Ísland að alþjóðlegri fjármálamiðstöð,"

Staðfest af Bankasýslunni, að innlendur starfsmannafj. sé svipaður og 2007 - þ.e. þegar starfsmfj. náði hámarki eftir hraða þenslu í fj. starfsmanna meðan bóluhagkerfið var að blása upp, frá 2004 fran að hruni október 2007. Einungis virðist hafa fækkað um starfsm. SPRON - starfsemi þess banka er lagðist að stórum hluta niður.

Eins og kemur fram á bls. 34 í annarri endurskoðunar-skýrslu AGS, sjá hlekk að neðan, er stærð endurreists bankakerfis á Íslandi, 159% af áætlaðri stærð hagkerfisins.

- Staðfest er sem sagt, að bankakerfið sé enn alltof stórt.

- Þetta verður að laga.

- Því aupplásið umfang er augljóslega hít fyrir fjármagn, og alveg örugglega orsakaþáttur í vandræðum bankanna við það að finna fjármagn til að framkvæma nauðsynlegar afskriftir lána.

Niðurstaða

Staðfest er, að bankakerfið er alltof stórt miðað við aðstæður. Ljóst virðist að við erum að stefna í annað sinn fram af bjargbrún. En, jafnvel nú á elleftu stundu má vera að enn sé hægt að bjarga málum í horn. En, skjótra og ákveðinna aðgerða er þá þörf.

Núverandi stefna, að láta Hæstarétt skera úr um hverjir vextir hluta af lánasafni bankanna eiga að vera, er í besta falli biðleikur stjórnvalda. Hann gefur ekki mikinn viðbótar tíma.

Væntanlega mun Hæstiréttur staðfesta hið augljósa, þ.e. að engin lög heimili að víkja til hliðar vaxtaákvæðum gildandi samninga, þ.e. samningsvextir standi.

Sennilega er e-h til í því, að þá komist bankakerfið í vandræði. En, þetta er líka annað tækifæri til að framkvæma nauðsynlega endurskipulagningu bankamála hérlendis.

Þ.e. nauðsynlegt, að með þeim hætti verði unnið með þetta - þ.e. út frá þeirri forsendu, að lágmarka skaða fyrir almenning og hagkerfið. Það verður ekki gert með áframhaldi núverandi stefnu, heldur með uppskurði bankakerfisins og endurreisn þess stórlegs smækkaðs, en þá loks á styrkum fjárhagslegum grunni.

Framkvæma verður almennar aðgerðir fyrir skuldara, til að skapa frið innan samfélagsins, en einnig sem hluta af almenndum efnahags aðgerðum til að stuðla að hagvexti.

Kv.

Stjórnmál og samfélag | Breytt s.d. kl. 21:00 | Slóð | Facebook | Athugasemdir (2)

6.7.2010 | 20:13

Þurfum að átta okkur á, við stöndum á bjargbrún annars hruns!

Hvernig stendur á að við virðumst aftur komin að nokkurn veginn sama stað, og eftir hrun?

- Eins og ég sé það, þá liggja mistökin í því, að innlenda bankakerfið var endurreist, nokkurn veginn eins og það, rétt fyrir hrun. Þ.e. - fyrir utan SPRON er hrundi og margir misstu þar vinnuna - er innlenda bankakerfið nokkurn veginn með sama starfsmannafjölda og fyrir hrun, en höfum í huga að þá erum við að tala um útþaninn starfsm.fj. bóluhagkerfisins að slepptum þeim er störfuðu erlendis. Skv. tölum AGS, er bankakerfið í dag 1,59 falt hagkerfið.

- Allur þessi fj. umfram brína þörf, þiggur laun sem eru langt yfir lágmarkslaunum, en laun bankamanna eru tiltölulega góð. Að auki, er það rekstrar og stjórnunarkostnaður umfram brína þörf.

- Þetta er verulegur peningur, sem dæmi er stærsti hluti kostnaðar Ríkisspítala launakostnaður. Sjálfsagt er það út af fyrir sig göfugt markmið að halda fólki á launum, þannig að þeirra fjölskyldur hafi nóg að bíta og brenna. En, þennan pening hefði einnig verið hægt að nota til að sinna öðru og a.m.k. ekki minna göfugu markmiði.

Er þetta ekki einfaldlega peningurinn, sem hefði dugað fyrir 20% leiðinni, sem Framsóknarflokkurinn lagði til, um árið?

Var þetta ekki líka gróðinn, af færslu útlánapakka frá þrotabúum gömlu bankanna, yfir til þeirra nýju, á tuga prósenta afslætti? Þannig, að sá gróði er nú uppeyddur?

------------------------------

Varðandi núverandi deilu um gengistryggð lán, var eftirfarandi haft eftir Steingrími J., Fjármálaráðherra. Hann er eins og fram kemur, mikill líðræðissinni :)

Steingrímur J. og gengistryggð lán

Steingrímu"Steingrímur J. Sigfússon, fjármálaráðherra, segir mikilvægt að fá

botn í það sem fyrst hvernig fara eigi með gengistryggð lán. Hann

segir hins vegar að farið verði eftir tilmælum Seðlabankans og

Fjármálaeftirlitsins um 8,5% prósent vexti þangað til. Ráðherra segir

að andstaða almennings hafi ekki áhrif á málið..."

„AGS einskonar skuggastjórnandi“

Lilja Mósesdóttir, sem er formaður viðskiptanefndar,segir

Alþjóðagjaldeyrissjóðinn vera nokkurs konar skuggastjórnanda og

andstaða hans við almenna niðurfellingu íbúðalána endurómi í stefnu

ríkisstjórnarinnar.

Þ.s. Lilja sagði, virðist vera kjarni málsins, þ.e. að landinu sé í reynd stjórnað af AGS.

Skv. því sem mér hefur verið sagt er þekktum erlendum aðilum, þá er AGS "very inverstor friendly organization".

Þ.e. mikil kaldhæðni í því, að fyrsta eiginlega vinstristjórnin hérlendis, fari þráðbeint í það far, að reka sérhagsmuni fjármálamanna, eigenda fjármagns, og starfsmanna bankanna.

Á sama tíma, er hagsmunum almennings, vinnandi fólks, og barnafjölskylda, fórnað.

-------------------------------

Við sem erum ósátt, þurfum samt sem áður að hugsa upp, hvernig vandinn verður leystur:

- - því ef þ.e. raunverulega satt, eins og Viðskiptaráðherra, og nú Fjármálaráðherra, segja.

- Þá, er búið að eyða upp hagnaðinum af yfirfærslu lánapakkanna, frá þrotabúum hrundu bankanna, yfir í þá nýju

- Þá stöndum við frammi fyrir þeim grimma valkosti, að taka bankana niður í annað sinn - ef til vill?

Viðkomandi staðreyndum má ekki heldur gleyma:

- Peningar verða ekki heldur búnir til úr engu, þ.e. ef hagnaðinum hefur verið eytt, er sá peningur farinn fyrir fullt og fast.

- Þá er ef til vill eina leiðin sem eftir er, til að framkvæma þá niðurstöðu sem er skv. ísl. lögum, og að auki nauðsynlega afskrift annarra lána; að minnka bankakerfið um helming, og að auki afskrifa öll innlán fyrir umfram þak sem gæti verið sett á bilinu 3-5 milljón per reikning.

Þ.e. auðvitað ekki sanngjarnt í sjálfu sér, að ráðast að innlánseigendum, en því má ekki gleyma að innlán eru skuld bankans við sérhvern innlánseigenda - þ.e. innlán eru skuldameginn hjá bönkunum.

- Ef eignastaða bankanna er hrunin, þeir eiga ekki fyrir nauðsynlegum afskriftum, þá eru þeir pent gjaldþrota í reynd, sem einnig þíðir ekki er innistæða lengur fyrir hendi fyrir innlánunum - hafandi í huga, að líklega er að auki ríkið ófært til að endurtaka leikinn frá því síðast, og tryggja öll innlán óháð upphæð.

Niðurstaða

Við stöndum með öðrum orðum frammi fyrir valkostum, sem allir eru slæmir - og alveg sama hvað verður gert, úrlausn mála getur ekki annað en falið í sér það að einhverjir tapi.

- Einn valkosturinn, er þá að halda áfram núverandi stefnu, þ.e. neita að afksrifa, að ganga svo langt að brjóta landslög til að tryggja hagsmuni þeirra er starfa í bönkunum, þá á kostnað restarinnar af almenningi. Þetta virðist leið AGS og stj.v. - með þá Gylfa og Steingrím í fararbroddi.

- Annar væri, að fórna bankamönnum, þ.e. stórum hluta þeirra, einnig innlánseigendum er eiga umfram 3-5 milljónir, einnig hagsmunum eigenda bankanna, en þess í stað verði hægt að ná fram sátt við almenning með leiðréttingum lána niður í það far þ.s. þau voru fyrir hrun - eða langleiðina þangað. Ljóst er, að sú leið er í andstöðu AGS og fjármála-afla samfélagsins, og virðist ríkistj.

Ég efst um að fyrri leiðin sé fær, þ.e. Hæstiréttur muni í annað sinn einfaldlega dæma skv. landslögum, og þá standi lánafyrirtæki þau er fara eftir tilmælum stj.v. jafnvel frammi fyrir skaðabótamálum, fyrir utan önnur töp.

Þau hið minnsta taka áhættu ef þau kjósa að fylgja tilmælum stj.v. - er virðast brjóta landslög og ganga gegn dómi Hæstaréttar - þ.s. með því að gera þetta einungis að tilmælum, varpa stj.v. áhættunni af valinu yfir til þeirra, en væntanlega var sú leið valin vegna þess að innst inni vita stj.v. að spilið er tapað - en samt sem áður, velja þau þann biðleik að halda áfram.

Má reyndar vera, -að stj.v. skv. hótun Gylfa Magnússonar og Steingríms J. gagnvart almenningi- þá leitist við að færa kostnað af þeim aðgerðum á almenning, þ.e. stj.v. taki þann valkost að dæla skattfé í bankana, til að halda öllu á floti áfram óbreittu - sem augljóslega væri einn biðleikurinn enn, hækki svo skatta og aðrar álögur á móti - til þess væntanlega að gersamlega að kaffæra atvinnulífinu í sköttum. Síðan, reyni þau enn um skeið að halda áfram stefnunni, að neita að afskrifa. Reynt verði áfram að halda öllum bankamönnum í vinnu - er ekki klárt fyrir hverja ríkisstj. starfar? Bankamenn, fjármálamenn og AGS. Auðvitað, breytir slík aðgerð engu öðru en því, að hruninu verður frestað ef til vill nokkra mánuði í viðbót - þ.e. ef almenningur einfaldlega pent gerir ekki uppreisn og sparkar öllu klabbinu í burtu.

Seinni leiðin, sjá að ofan, verður alls ekki heldur auðveld, en hún mun fela í sér algera endurskipulagningu bankakerfisins, verulega fjölgun atvinnulausra þ.s. sennilega helmingur bankamanna a.m.k. verða atvinnulausir - en, hugsanlega á móti, verður hægt að ná sátt við almenning.

Kv.

4.7.2010 | 17:36

Hverjar eru ástæður þess, að bankakerfi Evrópu ramba á barmi þrots?

Ég fæ reglulega sent analísur frá bandaríska einka-stofnuninni Stratfor. Eins og gerist og gengur, eru þeirra analísur mis áhugaverðar

En, um daginn fékk ég þessa fyrir neðan.

- Að mínu mati, er hún svo frábær greining á grunnástæðum fyrir vanda bankakerfa Evrópu, að ég hef ákveðið að setja hana inn í þessa bloggfærslu.

Ég hvet ykkur endilega til, að hafa fyrir því, að lesa þetta í gegn.

-----------------------------------------Source of analyzis STRATFOR

Europe: The State of the Banking System (STRATFOR Analyzis)

ast six months, the eurozone has faced its biggest economic challenge to date — one sparked by the Greek debt crisis which has migrated to the rest of the monetary union. But well before the sovereign debt crisis, Europe was facing a full-blown banking crisis that did not seem any closer to being resolved than when it began in late 2008. With investors and markets focused on European governments’ debt problems, the banking issues have largely been ignored. However, the sovereign debt crisis and banking crisis have become intertwined and could feed off each other in the near future.

Analysis

July 1 is a milestone for eurozone banks, with 442 billion euros ($541 billion) worth of European Central Bank (ECB) loans coming due. The loans were part of the ECB’s one-year liquidity offering made in 2009, which was intended to help stabilize the banking system.

However, one year after the ECB provision was initially offered, the eurozone’s banks are still struggling, and now Europe’s banks must collectively come up with the cash roughly equivalent to Poland’s gross domestic product (GDP).

Fears regarding the potentially adverse consequences of removing ECB liquidity are gripping many European banks and, by extension, investors who were already panicked by the sovereign debt crisis in the Club Med countries (Greece, Portugal, Spain and Italy). These concerns are as much a testament to the severity of the eurozone’s ongoing banking crisis as to the lack of resolve that has characterized Europe’s handling of the underlying problems.

Origins of Europe’s Banking Problems

Europe’s banking problems precede the eurozone’s ongoing sovereign debt crisis and even exposure to the U.S. subprime mortgage imbroglio. The European banking crisis has its origins in two fundamental factors: euro adoption in 1999 and the general global credit expansion that began in the early 2000s. The combination of the two created an environment that inflated credit bubbles across the Continent, which were then grafted onto the European banking sector’s structural problems.

In terms of specific pre-2008 problems we can point to five major factors. Not all the factors affected European economies uniformly, but all contributed to the overall weakness of the Continent’s banking sector.

1. Euro Adoption and Europe’s Local Subprime Bubble

The adoption of the euro — in fact, the very process of preparing to adopt the euro that began in the early 1990s with the signing of the Maastricht Treaty — effectively created a credit bubble in the eurozone. As the adjacent graph indicates, the cost of borrowing in peripheral European countries (Spain, Portugal, Italy and Greece in particular) was greatly reduced due, in part, to the implied guarantee that once they joined the eurozone their debt would be as solid as Germany’s government debt.

In essence, euro adoption allowed countries like Spain access to credit at lower rates than their economies could ever justify based on their own fundamentals. This eventually created a number of housing bubbles across Europe, but particularly in Spain and Ireland (the two eurozone economies currently boasting the relatively highest levels of private-sector indebtedness). As an example, in 2006 there were more than 700,000 new homes built in Spain — more than the total new homes built in Germany, France and the United Kingdom combined, even though the United Kingdom was experiencing a housing bubble of its own at the time.

It could be argued that the Spanish case was particularly egregious because Madrid attempted to use access to cheap housing as a way to integrate its large pool of first-generation Latin American migrant workers into Spanish society. However, the very fact that Spain felt confident enough to attempt such wide-scale social engineering indicates just how far peripheral European countries felt they could stretch their use of cheap euro loans. Spain is today feeling the pain of a collapsed construction sector, with unemployment approaching 20 percent and with the Spanish cajas (regional savings banks) reeling from their holdings of 58.9 percent of the country’s mortgage market. The real estate and construction sectors’ outstanding debt is equal to roughly 45 percent of the country’s GDP.

2. Europe’s ‘Carry Trade’

“Carry trade” usually refers to the practice in which loans are taken in a low interest rate country with a stable currency and “carried” for investment in the government debt of a high interest rate economy. The European practice, which extended the concept to consumer and mortgage loans, was championed by the Austrian banks that had experience with the method due to their proximity to the traditionally low interest rate economy of Switzerland.

In the carry trade, the loans extended to consumers and businesses are linked to the currency of the country where the low interest loan originates. Because of this, Swiss francs and euros served as the basis for most of such lending across Europe. Loans in these currencies were then extended as low interest rate mortgages and other consumer and corporate loans in higher interest rate economies in Central and Eastern Europe. Since loans were denominated in foreign currency, when their local currency depreciated against the Swiss franc or euro, the real financial burden of the loan increased.

This created conditions for a potential economic maelstrom at the onset of the financial crisis in 2008 when consumers in Central and Eastern Europe saw their monthly mortgage payments grow as investors pulled out from emerging markets in order to “flee to safety,” leading these countries’ domestic currencies to fall. The problem was particularly dire for Central and Eastern European countries with a great amount of exposure to such foreign currency lending (see adjacent table).

3. Crisis in Central/Eastern Europe

The carry trade led Europe’s banks to be overexposed to Central and Eastern European economies. As the European Union enlarged into the former Communist sphere in Central Europe, and as security and political uncertainties in the Balkans subsided in the early 2000s, European banks sought new markets where they could make use of their expanded access to credit provided by euro adoption. Banking institutions in mid-level financial powers such as Sweden, Austria, Italy and even Greece sought to capitalize on the carry trade by going into markets that their larger French, German, British and Swiss rivals largely shunned.

This, however, created problems for the banking systems that became overexposed to Central and Eastern Europe. The International Monetary Fund and the European Union ended up having to bail out several countries in the region, including Romania, Hungary, Latvia and Serbia. And before the eurozone ever contemplated a Greek or eurozone bailout, it was discussing a potential 150 billion-euro rescue fund for Central and Eastern Europe at the urging of the Austrian and Italian governments.

4. Exposure to ‘Toxic Assets’

The exposure to various credit bubbles ultimately left Europe vulnerable to the financial crisis, which peaked with the collapse of Lehman Brothers in September 2008. But the outright exposure to various financial derivatives, including the U.S. subprime market, was by itself considerable.

While the Swedish, Italian, Austrian and Greek banking systems expanded into the new markets in Central and Eastern Europe, the established financial centers of France, Germany, Switzerland, the Netherlands and the United Kingdom dabbled in various derivatives markets. This was particularly the case for the German banking system, where the Landesbanken — banks with strong ties to regional governments — faced chronically low profit margins caused by a fragmented banking system of more than 2,000 banks and a tepid domestic retail banking market. The Landesbanken on their own face between 350 billion and 500 billion euros worth of toxic assets — a considerable figure for the 2.5 trillion-euro German economy — and could be responsible for nearly half of all outstanding toxic assets in Europe.

5. Demographic Decline

Another problem for Europe is that its long-term outlook for consumption, particularly in the housing sector, is dampened by the underlying demographic factors. Europe’s birth rate is at 1.53, well below the population “replacement rate” of 2.1. Exacerbating the demographic imbalance is the increasing life expectancy across the region, which results in an older population. The average European age is already 40.9, and is expected to hit 44.5 by 2030.

An older population does not purchase starter homes or appliances to outfit those homes. And if older citizens do make such purchases, they are less likely to depend as much on bank lending as first-time homebuyers. That means not just less demand, but that any demand will depend less upon banks, which means less profitability for financial institutions. Generally speaking, an older population will also increase the burden on taxpayers in Europe to support social welfare systems, dampening consumption further.

In this environment, housing prices will continue to decline (barring another credit bubble, which would of course exacerbate problems). This will further restrict lending activities because banks will be wary of granting loans for assets that they know will become less valuable over time. At the very least, banks will demand much higher interest rates for these loans, but that too will further dampen the demand.

The Geopolitics of Europe’s Banking System

Given these challenges, the European banking system was less than rock-solid even before the onset of the global recession in 2008. However, Europe’s response as a Continent to the crisis so far has been muted, with essentially every country looking to fend for itself. Therefore, at the heart of Europe’s banking problems lie geopolitics and “capital nationalism.”

Europe’s geography encourages both political stratification and unity in trade and communications. The numerous peninsulas, mountain chains and large islands all allow political entities to persist against stronger rivals and continental unification efforts, giving Europe the highest global ratio of independent nations to area. Meanwhile, the navigable rivers, inland seas (Black, Mediterranean and Baltic), Atlantic Ocean and the North European Plain facilitate the exchange of ideas, trade and technologies among the disparate political actors.

This has, over time, incubated a continent full of sovereign nations that intimately interact with one another but are impossible to unite politically. Furthermore, in terms of capital flows, European geography has engendered a stratification of capital centers. Each capital center essentially dominates a particular river valley where it can use its access to a key transportation route to accumulate capital. These capital centers are then mobilized by the proximate political powers for the purposes of supporting national geopolitical imperatives, so Viennese bankers fund the Austro-Hungarian Empire, for example, while Rhineland bankers fund the German Empire. With no political unity, the stratification of capital centers becomes more solidified over time.

The European Union’s common market rules stipulate the free movement of capital across the borders of its 27 member states. Theoretically, with barriers to capital movement removed, the disparate nature of Europe’s capital centers should wane; French banks should be active in Germany, and German banks should be active in Spain. However, control of financial institutions is one of the most jealously guarded privileges of national sovereignty in Europe.

One reason for this “capital nationalism” is that Europe’s corporations and businesses are far less dependent on the stock and bond market for funding than their U.S. counterparts, relying primarily on banks. This comes from close links between Europe’s state champions in industry and finance (for example, the close historical links between German industrial heavyweights and Deutsche Bank). Such links, largely frowned upon in the United States for most of its history, were seen as necessary by Europe’s nation-states in the late 19th and early 20th centuries because of the need to compete with industries in neighboring states. European states in fact encouraged — in some ways even mandated — banks and corporations to work together for political and social purposes of competing with other European states and providing employment. This also goes for Europe’s medium-sized businesses — Germany’s mid-sized businesses are a prime example — which often rely on regional banks they have political and personal relationships with.

Regional banks are an issue unto themselves. Many European economies have a special banking sector dedicated to regional banks owned or backed by regional governments, such as the German Landesbanken or the Spanish cajas which in many ways are used as captive firms to serve the needs of both the local governments (at best) and local politicians (at worst). Many Landesbanken actually have regional politicians sitting on their boards while the Spanish cajas have a mandate to reinvest around half of their annual profits in local social projects, tempting local politicians to control how and when funds are used.

Europe’s banking architecture was therefore wholly unprepared to deal with the severe financial crisis that hit in September 2008. With each banking system tightly integrated into the political economy of each EU member state, an EU-wide “solution” to Europe’s banking problems — let alone the structural issues, of which the banking problems are merely symptomatic — has largely evaded the Continent. While the European Union has made progress in enhancing EU-wide regulatory mechanisms by drawing up legislation to set up micro- and macro-prudential institutions (with the latest proposal still in the implementation stages), the fact remains that outside of the ECB’s response of providing unlimited liquidity to the eurozone system, there has been no meaningful attempt to deal with the underlying structural issues on the political level.

EU member states have, therefore, had to deal with banking problems largely on a case-by-case (and often ad hoc) basis, as each government has taken extra care to specifically tailor its financial assistance packages to support the most and upset the fewest constituents. In contrast, the United States — which took an immediate hit in late 2008 — bought up massive amounts of the toxic assets from the banks, swiftly transferring the burden onto the state.

Europe’s banking system obviously has problems, but exacerbating the problems is the fact that Europe’s banks know that they and their peers are in trouble. This is causing the interbank market to seize up and thus forcing Europe’s banks to rely on the ECB for funding.

The interbank market refers to the wholesale money market that only the largest financial institutions are able to participate in. In this market, the participating banks are able to borrow from one another for short periods of time to ensure that they have enough cash to maintain normal operations. Normally, the interbank market essentially regulates itself. Banks with surplus liquidity want to put their idle cash to work, and banks with a liquidity deficit need to borrow in order to meet the reserve requirements at the end of the day, for example. Without an interbank market there is no banking “system” because each individual bank would be required to supply all of its own capital all the time.

In the current environment in Europe, many banks are simply unwilling to lend money to each other, as they do not trust their peers’ creditworthiness, even at very high interest rates. When this happened in the United States in 2008, the Federal Reserve and Federal Deposit Insurance Corporation stepped in and bolstered the interbank market directly and indirectly by both providing loans to interested banks and guaranteeing the safety of the loans banks were willing to grant each other. Within a few months, the U.S. crisis mitigation efforts allowed confidence to return and this liquidity support was able to be withdrawn.

The ECB originally did something similar, providing an unlimited volume of loans to any bank that could offer qualifying collateral, while national governments offered their own guarantees on newly issued debt. But unlike in the United States, confidence never fully returned to the banking sector due to the reasons listed above, and these provisions were never canceled. In fact, this program was expanded to serve a second purpose: stabilizing European governments.

With economic growth in 2009 weak, many EU governments found it difficult to maintain government spending programs in the face of dropping tax receipts. They resorted to deficit spending, and the ECB (indirectly) provided the means to fund that spending. Banks could purchase government bonds, deposit them with the ECB as collateral and walk away with a fresh liquidity loan (which they could use, if they so chose, to buy yet more government debt).

The ECB’s liquidity provisions were ostensibly a temporary measure that would eventually be withdrawn as soon as it was no longer necessary. So on July 1, 2009, the ECB offered the first of what was intended to be its three “final” batches of 12-month loans as part of a return to a more normal policy. On that day 1,121 banks took out a record total of 442 billion euros in liquidity loans (followed by another 75 billion euros taken out in September and 96 billion euros in December). The 442 billion euro operation has come due July 1. The day before, banks tapped the ECB’s shorter-term liquidity facilities to gain access to 294.8 billion euros to help them bridge the gap.

Europe now faces three problems:

- First, global growth has not picked up sufficiently in the last year, so European banks have not had a chance to grow out of their problems. This would have been difficult to accomplish on such a short timeframe.

- Second, the lack of a unified European banking regulator — although the European Union is trying to set one up — means that there has not yet been any pan-European effort to fix the banking problems. And even the regulation that is being discussed at the EU-level is more about being able to foresee a future crisis than resolving the current one. So banks still need the emergency liquidity provisions now as they did a year ago (to some degree the ECB saw this coming and has issued additional “final” batches of long-term liquidity loans). In fact, banks remain so unwilling to lend to one another that they have deposited nearly the equivalent amount of credit obtained from ECB’s liquidity facilities back into its deposit facility instead of lending it out to consumers or other banks.

- Third, there is now a new crisis brewing that not only is likely to dwarf the banking crisis, but could make solving the banking crisis impossible. The ECB’s decision to facilitate the purchase of state bonds has greatly delayed European governments’ efforts to tame their budget deficits. There is now nearly 3 trillion euros of outstanding state debt just in the Club Med economies — vast portions of which are held by European banks — illustrating that the two issues have become as mammoth as they are inseparable.

There is no easy way out of this imbroglio. Reducing government debts and budget deficits means less government spending, which means less growth because public spending accounts for a relatively large portion of overall output in most European countries. Simply put, the belt-tightening that Germany and the markets are forcing upon European governments likely will lead to lower growth in the short term (although in the long term, if austerity measures prove credible, it should reassure investors of the credibility of the eurozone’s economies). And economic growth — and the business it generates for banks — is one of the few proven methods of emerging from a banking crisis. One cannot solve one problem without first solving the other, and each problem prevents the other from being approached, much less solved.

There is, however, a silver lining. Investor uncertainty about the European Union’s ability to solve its debt and banking problems is making the euro ever weaker, which ironically will support European exporters in the coming quarters. This not only helps maintain employment (and with it social stability), but it also boosts government tax receipts and banking activity — precisely the sort of activity necessary to begin addressing the banking and debt crises. But while this might allow Europe to avoid a return to economic recession in 2010, it alone will not resolve the European banking system’s underlying problems.

For Europe’s banks, this means that not only will they have to write down remaining toxic assets (the old problem), but they now also have to account for dampened growth prospects as a result of budget cuts and lower asset values on their balance sheets due to sovereign bonds losing value.

Ironically, with public consumption down as a result of budget cuts, the only way to boost growth would be for private consumption to increase, which is going to be difficult with banks wary of lending.

The Way Forward?

So long as the ECB continues to provide funding to the banks — and STRATFOR does not foresee any meaningful change in the ECB’s posture in the near term or even long term — Europe’s banks should be able to avoid a liquidity crisis. However, there is a difference between being well-capitalized but sitting on the cash due to uncertainty and being well-capitalized and willing to lend. Europe’s banks are clearly in the former state, with lending to both consumers and corporations still tepid.

In light of Europe’s ongoing sovereign debt crisis and the attempts to alleviate that crisis by cutting down deficits and debt levels, European countries are going to need growth, pure and simple, to get out of the crisis. Without meaningful economic growth, European governments will find it increasingly difficult — if not impossible — to service or reduce their ever-larger debt burdens. But for growth to be engendered, the Europeans are going to need their banks, currently spooked into sitting on liquidity, to perform the vital function that banks normally do: finance the wider economy.

As long as Europe faces both austerity measures and reticent banks, it will have little chance of producing the GDP growth needed to reduce its budget deficits. If its export-driven growth becomes threatened by decreasing demand in China or the United States, it could also face a very real possibility of another recession which, combined with austerity measures, could precipitate considerable political, social and economic fallout.

---------------------------------------------------Analyzis from STRATFOR.

Að mínu mati frábær analía.

Kv.

3.7.2010 | 09:20

Ríkissjóður Íslands er með hæstu vaxtagreiðslur sem hlutfall af eigin tekjum, af ríkissjóðum allra OECD ríkja!

Gylfi Magnússon, hefur margítrekað borið stöðu ríkissjóðs Íslands saman við stöðu ríkissjóða annarra Evrópulanda, ekki síst stöðu Bretlands, og ályktað að skuldastaða ríkissjóðs Íslands sé ekki ósambærileg - eða, ekki að ráði verri.

- Ályktunin sem hann hefur af því dregið, hefur verið sú að íslenska ríkið muni ráða við sínar skuldir!

- Vandinn við þetta er að - viðmiðið, skuldir sem hlutfall af landsframleiðsu - segir í raun og veru ekki nema hluta af sögunni.

Þ.s. skiptir meira máli, er hver akkúrat vaxtagjöld eru sem hlutfall af tekjum, enda líkur á að lönd séu að greiða misháa vexti af sínum skuldum, sem dæmi er líklegt að Bretland sé að fá betri vaxtakjör en litla Ísland. Óhagstæð vaxtakjör að sjálfsögðu skekkja myndina, þannig að ríki með lægra skuldahlutfall getur verið með hærri vaxtagjöld samt sem áður, ef lán eru óhagstæð.

Hérna fyrir neðan er samanburðartafla skv. upplýsingum frá OECD þ.s. fram kemur samanburður milli ríkja á vaxtagjöldum eftir árum.

- Þar kemur klárlega fram, að vaxtagjöld Íslands eru hæst - sem þíðir að Ísland er með erfiðustu raun-skuldastöðu allra ríkja innan OECD, því Ísland er með hæsta kostnaðinn af sínum skuldum.

- Takið eftir, að okkar vaxtagjöld eru verulega hærri en vaxtagjöld Grikklands, sem Þó allir eru sammála um í dag, að sé gjaldþrota land.

En, eins og kemur einnig skýrt þarna fram, er megnið af skuldunum komnar til fyrir tilverknað hrunsins, og ef fólk hefur verið að fylgjast með þá er einmitt vandi okkar, þ.e. eitt af vandamálunum, að stór lán voru tekin á mjög óhagstæðum tíma mitt í alþjóðlegu fjármálakreppunni, þegar lánakjör voru mjög óhagstæð - og enduðum við því með há lán á mjög dýrum kjörum - t.d. lánið til endurfjármögnunar Seðlabanka. Við áttum því miður ekkert val um annað, þegar í óefni var komið, en að taka þau óhagstæðu lán.

- Afleiðingin er - eins og kemur fram að neðan - mjög há vaxtagjöld.

Vandinn við svo há vaxtagjöld, er að þar með hefur ríkið minna fé til að standa undir nauðsynlegri þjónustu, og til að reka sjálft sig - og að auki, minna til að standa undir uppbyggingu í framtíðinni.

Alex Jurshevski - sagði á eigin bloggi, sjá " Why Iceland Must Vote “No” " - Um AGS lánapakkann, að "If the package were to be adopted the share of debt servicing out of total government revenues would top 16%. At those levels this statistic is more usually associated with extreme sovereign default risk. "

Þ.s. hann er að vísa til, að þ.e. mjög erfitt að búa við það að svo hátt hlutfall ríkistekna fari beint úr landi, engum í landinu til góðs. Rekstur við slíkar aðstæður, verður mjög erfiður.

Alex Jurshevski á Pressunni, segir "Evrópa vaknar upp við vondan skuldadraum...er Ísland ennþá sofandi?" - Við skoðun á meira en 140 tilraunum til þess að draga saman ríkisútgjöld í þróuðum ríkjum OECD koma nokkrar niðurdrepandi staðreyndir í ljós:

 Í meirihluta tilvika var farið í flatan niðurskurð þar sem fjárlög voru skyndilega skorin niður um 1-4% af vergri landsframleiðslu á einu ári. Þetta er svipað og gert hefur verið á Íslandi frá 2008.

 Í flestum tilvikum batnaði fjárhagsstaðan aðeins um 2% af vergri landsframleiðslu (miðgildi niðurstaðna) og í flestum tilvikum varði aðhaldið aðeins í tvö ár; og

 næstum 66% af niðurskurðaraðgerðunum voru álitnar misheppnaðar og í flestum tilvikum hafði árangurinn að mestu leyti horfið innan þriggja ára.

Jurshevski bendir á að flatur niðurskurður, sé mjög gölluð aðferð:

- En, sem dæmi, ef stofnanir eru skikkaðar til að skera niður t.d. 6% þetta árið, 4% næsta - sem dæmi, þá er hætta á að því sé einfaldlega komið í framkvæmd með því einu, að fresta endurnýjun tækja, viðhaldi húseigna - ímsu slíku sem auðvelt er að fresta tímabundið, - en slíkt er ekki raunverulegur sparnaður.

- Ef slíkum aðferðum er beitt, þá eðlilega sækir kostnaður aftur í sama farið innan fárra ára, þegar ekki er lengur hægt að fresta þeim þáttum, er tímabundið voru settir í frest.

- Raunverulegur niðurskurður sé þolinmæðisvinna, þ.s. vanalega er um þörf á skipulagsbreytingum að ræða.

- Fyrir utan þetta, er einna helst um það að velja, að hreinlega að leggja einhverja starfsemi niður.

Einst og sést að ofan, til að standa undir hinni gríðarlegu hækkun vaxtagjalda:

- Til samanburðar stendur til að ríkissjóður Grikklands nái inn minnkun upp á um 11%.

- Með enn hærri vaxtagjöld, þá hlýtur að þurfa að spara hærra hlutfall hérlendis.

IMF Reaches Staff-level Agreement with Greece on €30 Billion Stand-By Arrangement

A combination of spending cuts and revenue increases amounting to 11 percent of GDP—on top of the measures already taken earlier this year—are designed to achieve a turnaround in the public debt-to-GDP ratio beginning in 2013 and will reduce the fiscal deficit to below 3 percent of GDP by 2014.

Niðurstaða:

Við Íslendingar þurfum að horfast í augu við það, að Íslendingar allir - og hið opinbera, verða á næstu árum, að rifa seglin og það sem um munar.

- Flatur niðurskurður, getur einungis verið skammtíma neyðaraðgerð.

- Síðan, þarf að taka við úthugsaðar aðgerðir, sem lúta að því að ná fram sparnaði með skipulagsbreytingum.

- En, einnig þurfum við að sætta okkur við, að það verður nauðsynlegt að leggja niður margvíslega starfsemi og þjónustu á vegum ríkisins og hins opinbera, og sennilega skerða þjónustu að auki.

- Fyrir utan þetta, verða Íslendingar sennilega fyrir frekari samdrætti í lífskjörum.

Alls engin innistæða er fyrir launahækkunum á næstu misserum, hvorki hjá ríkinu né hinu opinbera, og líklega ekki heldur hjá atvinnulífinu.

- Draumar um að sækja aftur til baka þau lífskjör er tapast hafa, verða að bíða betri tíma - en, mjög sennilega, mun það taka langan tíma að ná þeim hápunkti hvað lífskjör varðar.

Fyrir utan sparnað, verður að hrinda í framkvæmd aðgerðum, sem hjálpa atvinnulífinu og almenningi að rétta við sér.

- Lækkum vexti, og það stórlega, niður í 1%. Engin ein aðgerð mun skila meiri hagsbótum fyrir hag heimila og fyrirtækja.

- Hvetjum einnig til útflutnings, með skattaívilnunum til þeirra er annað af tvennu, vilja hefja nýja útflutningsstarfsemi, eða, hyggja á að umbreyta fyrri starfsemi sinni í það horf að þaðan í frá skapi hún gjaldeyristekjur.

Þessar aðgerðir, ættu alveg að geta dugað til að skapa sjálfssprottinn hagvöxt.

- Að auki vil ég leggja af verðtryggingu, þ.s. hún er mjög skaðlegt fyrirbæri fyrir hagkerfið, m.a. dregur hún úr virkni vaxtatækisins við hagstjórn og að auki hvetur hún til áhættusækni þeirra er veita lán. Að auki, bitnar hún mjög á almenningi.

- Síðan, þarf að finna leið til að afskrifa sem mest af lánum, ég vil eina stóra almenna afskrift - segjum 30-35%.

Ásamt lækkun vaxta, og líklegu raunverulegu upphafi hagvaxtar, þá ættu þær aðgerðir að duga almenningi til þess, að hann fari að sjá einhverja vonarglætu í sortanum.

Kv.

Stjórnmál og samfélag | Breytt s.d. kl. 11:54 | Slóð | Facebook | Athugasemdir (0)

1.7.2010 | 23:05

Nú hafa tveir Nóbelsverðlaunahafar tjáð sig um krónuna, þ.e. Paul Krugman og Joseph Eugene Stiglitz, og sagt hana gera okkur meira gagn en ógagn!

Tveir Nóbelsverðlaunahafar í hagfræði, hafa nú tjáð sig um málefni Íslands og sagt krónuna gera okkur meira gagn en ógagn.

Hlustið á Stiglitz: Stiglitz í Háskóla Íslands, fyrirspurnartími ásamt öðrum hagfr.

En, einhvern veginn, reikna ég samt ekki með því að sannfærðir innan Samfylkingarinnar, skipti um skoðun :)

Sjáum hvað Krugman segir: The Icelandic Post-crisis Miracle

"Unlike other disaster economies around the European periphery – ...Iceland devalued its currency massively and imposed capital controls."

"And a strange thing has happened: although Iceland is generally considered to have experienced the worst financial crisis in history, its punishment has actually been substantially less than that of other nations."

-------------------------------------------------Töflurnar af blogginu hans Krugman

Sjá: The Icelandic Post-crisis Miracle

Eurostat

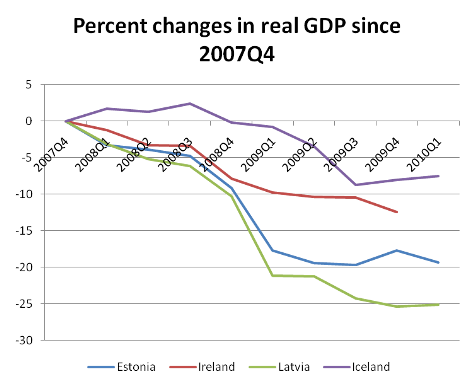

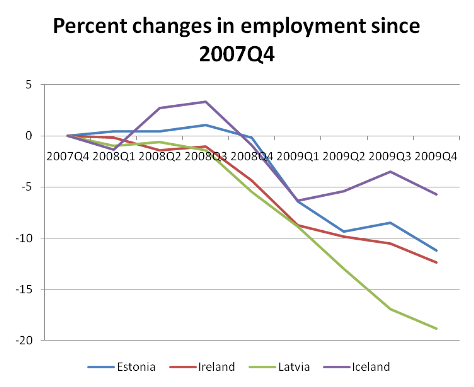

Eurostat- Þessi tafla sýnir, að samdráttur í landsframleiðslu var langminnstur á Íslandi.

Eurostat

Eurostat- Þessi tafla sýnir að aukning atvinnuleysis var langminnst á Íslandi.

---------------------------------------------------------------Innskoti lokið

Til áréttingar þess sem þegar er komið fram, vil ég aftur vekja athygli á niðurstöðum sérfræðings hjá "Bank of International Settlements", þ.e. greining á efnahagslegum afleiðingum stórfelldra gengisfellinga.

Þessi kafli, er undirkafli í nýjustu ársfjórðungsskýrslu "Bank of International Settlements".

"Currency collapses and output dynamics: a long-run perspective"

Sjá hlekk: Quarterly Review - June 2010

Um rannsóknina:

- "This article presents new evidence on the relationship between currency collapses,,,and real GDP."

- "The analysis is based on nearly 50 years of data covering 108 emerging and developing economies."

- "...we identify a total of 79 episodes (Table 1). The threshold for a depreciation to qualify as a currency collapse is around 22%..."

Helstu niðurstöður:

- "We find that output growth slows several years before a currency collapse, resulting in

sizeable permanent losses in the level of output."

- "On average, real GDP is around 6% lower three years after the event than it would have been otherwise."

- "However, these losses tend to materialise before the currency collapse."

- "This means that the economic costs do not arise from the depreciation per se but rather reflect other factors."

- "Quite on the contrary, depreciation itself actually has a positive effect on output."

- Growth tends to pick up in the year of the collapse and accelerate afterwards.

- Growth rates a year to three years after the episode are on average well above those one or two years prior to the event.

Hvað með Ísland og krónuna?

Eins og kemur mjög skýrt fram að ofan, kemur vandinn fram áður en stór gengisfelling á sér stað -þ.e. atburðir er eiga sér stað á undan eru raunorsök.

- Á Íslandi hafði gengi krónunnar hækkað óeðlilega mikið - verið óeðlilega hátt um nokkur ár og að auki frá cirka 2004 til október 2008 var til staðar bóluhagkerfi í stöðugri útþenslu sem gat að sjálfsögðu ekki gengið upp - þannig að ljóst er að gengishrunið var ekki orsök kreppunar sem skall á heldur rökrétt afleiðing hruns bóluhagkerfisins.

Síðan, hjálpar gengisfellingin hagkerfinu í því að rétta úr kútnum, þ.e. gengisfellingin flýtir fyrir að hagkerfið nái sér af áfallinu.

- Ég held að það sé alveg klárt einnig af gögnunum frá Krugman, að gengisfall krónunnar hefur hjálpað hagkerfinu.

En, er þá ekki krónan ónýt?

Við verðum að muna, að gjaldmiðillinn hvílir á grunni hins undirliggjandi hagkerfis. Með öðrum orðum, ef hagkerfið er traust er gjaldmiðillinn traustur, og öfugt. Svo, þá er fólk beinlínis að segja að ísl. hagkerfið sé ónýtt.

En þ.e. alls ekki satt, en þ.s. hérlendis eru enn flutt út verðmæti þ.e. ál og fiskur, að auki höfum við tekjur af ferðamönnum; þá er hér enn starfandi hagkerfi. Þannig, að gjaldmiðillinn sem á því hvílir, getur ekki á meðan svo er, orðið verðlaus.

Grunnvandi krónunnar liggur í því að ísl. hagkerfið hefur verið sveiflukennt og að auki í því að ísl. hagstjórn hefur of oft verið fremur léleg, þannig að í stað þess að tempra sveiflur hefur hún magnað þær - sem hefur þá byrst í genginu sem stórar gengissveiflur.

Að auki, er einnig vandi í sjálfu eðli okkar framleiðsluhagkerfis, þ.e. einhæft - útflutningurinn einhæfur.

- Gengissveiflur verða oftast þannig, að sveiflur verða í hagkerfinu.

- Leiðin, til að minnka sveiflurnar, er að breyta sveiflutíðni sjálfs hagkerfisins - sem þá gerir einnig krónuna stöðugari - reyndar mun það einnig skapa þau hliðaráhrif að gera það auðveldara að búa við annan gjaldmiðil en krónu.

- Að auki, þurfum við að bæta hagstjórn - það lítur að innlendum stjórnmálum og þeim stofnunum sem hér hafa verið upp byggðar.

Sjúkdómsgreiningin er sem sagt sú, að gengissveiflur séu einkenni sjúkdóms sem eigi rót til sjálfs grunnsins er allt hvílir á, þ.e. framleiðsluhagkerfið - annars vegar - og hins vegar, í landstjórninni.

Réttur skilningur, er síðan forsenda fyrir því að komast að réttum lausnum.

- Pólitíkina þurfum við einfaldlega að laga, bæta vinnubrögð.

Hverskonar framleiðsluhagkerfi, þrifust innan Evrunnar?

Þetta þarf aðeins að skoða gagnrýnum augum, þ.e. fyrir hvaða hagkerfi Evran hefur virkað hvað best - þ.e. hagkerfi sem selja dýra hátækni vöru fyrir mikinn pening per tonn.

Af hverju er það atriði? Þ.e. vegna þess, að ef þú færð mikinn virðisauka fyrir þinn útflutning, þ.e. varan á endanum verður mjög mikið verðmætari en þ.s. fer í hana af hráefnum, þá skiptir sjálft verðið á gjaldmiðlinum ekki lengur höfuðmáli fyrir þinn útflutning þ.e. samkeppnishæfni hans, einmitt vegna þess að verðið á gjaldmiðlinum er þá svo lítill hluti heildarverðmætaaukningar hráefnanna.

Þannig, að þá ber þitt framleiðsluhagkerfi dýran gjaldmiðil og það án vandkvæða.

Íslenska framleiðsluhagkerfið er mjög viðkvæmt fyrir kostnaðarhækkunum!

Þ.e. aftur á móti mjög klárt, oftlega sannað með dæmum þ.s. krónan hækkar og útflutningi hnignar - innflutningur verður meiri að verðmætum; að ísl. framleiðsluhagkerfið er mjög viðkvæmt fyrir verðinu á gjaldmiðlinum.

- Höfum í huga, að í stað þess að okkar aðalútflutningur sé dýr tæki og aðrar hátæknivörur, er hann ferskfiskur að mestu óunninn og ál (þ.e. ekki vörur úr áli) - svo höfum við ferðamenn.

- Þ.s. ég er að reyna að segj, er að frumstæði okkar framleiðsluhagkerfis sé þarna til vansa, sem sést m.a. annars á lærdómi S-Evrópu af því að búa við Evru.

En, ástæða þess að framleiðsluhagkerfum margra Evru-ríkja hnignaði undir Evrunni, er hún hækkaði í verði - var akkúrat sú, að eins og útflutningur Íslands, er útflutningur þeirra landa einnig á mun lægra virðisaukastigi verðmætalega en t.d. útflutningur Þýskalands.

Þetta er atriði sem þarf að skoða af mikilli alvöru, en eins og ég skil þetta, þ.s. Evran miðast við Þýskaland og þ.s. Ísl. framleiðsluhagkerfið er miklu mun vanþróaðra, þá gildir eftirfarandi:

- Laun hér verða alltaf að vera lægri en í Þýskalandi, í samræmi við að hvaða marki virðisauki per tonn er lægri hér á landi.

- Vegna þess, hve okkar framleiðsluhagkerfi hnignar hratt ef innlendur kostnaður hækkar, verða laun að lækka hérlendis eftir því sem Evran hækkar í verðgildi.

- Laun má hækka, ef Evran lækkar.

- Laun má ekki hækka umfram aukningu framleiðni í hagkerfinu, sem á síðasta áratug var cirka 1,5% á ári.

Höfum í huga, að þetta er mjög erfið spennitreyja - að auki, að löndunum sem nú eru í vandræðum Evrópu, sem lentu í vítahring vaxandi viðskiptahalla og skuldasöfnunar, þeim tókst ekki að auðsýna aga af þessu tagi - þannig að þetta er raunverulega mjög - mjög erfitt í framkvæmd.

Höfum að auki í huga, að til þess að þetta gangi upp, verða allir að spila með og þ.e. ríkið, sveitarfélög og aðilar vinnumarkaðarins. Þ.e. ekki síst þ.s. er erfitt.

Ekki má heldur gleyma þeim pólitíska vanda og stjórnkerfisvanda, sem hér hefur afhjúpast.

*******Ég hef ekki trú á að þetta sé hægt í framkvæmd.*******

Niðurstaða

Mynnumst þess, að tveir Nóbelsverðlaunahafar hafa nú tjáð sig, og bent okkur á að krónan þrátt fyrir marga galla, sé samt að vinna okkur gagn.

Mynnumst einnig krísunnar í S-Evrópu, þ.s. land eftir landi, hefur lent í svipuðum efnahagsvanda að ímsu leiti og Ísland; þ.e. viðskiptahalla - skuldasöfnun, bæði fyrirt. og almennings.

Minn lærdómur af krísunni í Evrópu tengdri Evrunni, er sem sagt sá að þrátt fyrir alla galla - sem trúið mér ég þekki þá alla - sé enn meira gallað fyrir okkur, að búa við annan gjaldmiðil en krónu; svo lengi sem okkar framleiðsluhagkerfi er hvort tveggja í senn einhæft og "low tech".

Okkar innlenda stjórnkerfis- og stjórnmálavanda, verðum við einnig að leysa. Annars er hann sjálfstætt efnahags vandamál.

Ég er að segja, að þeir sem gagnrýndu Evrópu út frá þeirri forsendu, að Evrópa væri ekki "optimal currency area" vegna þess hve stór munur væri á milli innbyrðis samkeppnishæfni hagkerfa hennar, hafi haft rétt fyrir sér. Að auki, er ég að segja að Ísland sé klárlega í lélega hópnum, þ.e. að það sama eigi við um okkur, að Evran henti okkur ekki, né virðist sem hún henti S-Evrópu.

Svo þarf ekki að vera um aldur og æfi. Við getum breytt þessu. Gert okkar hagkerfi samkeppnishæft við þróuð hagkerfi, og að því eigum við að stefna. Við getum hugsanlega haft þ.s. langtímamarkmið, að taka upp annan gjaldmiðil - sem við ráðum ekki yfir - t.d. 20 ára plan.

Sko, það sama og gerir okkur auðveldar um vik, að lifa áfram við krónuna, mun einnig skapa skilyrði fyrir því að taka upp annan gjaldmiðil. Það verður þá einfaldlega valkostur, A eða B.

- Það þarf að hefja allsherjar og langtímaátak, til að bæta framleiðsluhagkerfið.

- Það gengur ekki lengur, að hafa framleiðsluhagkerfið sambærilegt við S-Evrópu og á sama tíma reyna að halda uppi sama þjónustustigi og á Norðurlöndum.

- Ég er hræddur um, að við verðum að færa þjónustustig niður á það plan sem framleiðsluhagkerfið í reynd stendur undir - og síðan gera það að langtímaplani svona 20 ára plani, að komast til baka.

- Síðast en ekki síst, bæta innlenda stjórnsýslu og stjórnun af hendi okkar stjórnmála á hagkerfinu.

Kv.

Stjórnmál og samfélag | Breytt 2.7.2010 kl. 22:08 | Slóð | Facebook | Athugasemdir (3)

Um bloggið

Einar Björn Bjarnason

Efni

Nýjustu færslur

- Gæti 3ja heimsstyrrjöldin hafist á Indlandshafssvæðinu? Skv. ...

- Er samningur Trumps við Japan - er inniber 550 milljarða$ fjá...

- Hótel-bókanir í sumar, gefa vísbendingar um kjaraskerðingu al...

- Kjarnorkuáætlun Írana hefur líklega beðið stórtjón, fremur en...

- Netanyahu, virðist hafa hafið stríð við Íran - beinlínis til ...

- Trump ákveður að senda, Landgönguliða - til Los-Angeles! Kemu...

- Möguleiki að Úkraína hafi í djarfri árás á flugvelli sumir mö...

- Yfirlýsing Trumps um yfirvofandi 50% tolla á ESB lönd, afhjúp...

- Tollar Bandaríkjanna á Kína - líklega ca: 50%. Kína á Bandarí...

- Að það verður af hráefnasamningi Úkraínu og Bandaríkjanna - v...

- Margt bendi til yfirvofandi kreppu í Bandaríkjunum! Skv. áhug...

- Vaxandi líkur á að Trump, reki: Jerome Powell. Yfirmann Seðla...

- Gideon Rachman hjá Financial Times -- útskýrir af hverju, Ban...

- Trump undanskilur frá tollum á Kína -- snjallsíma, og nánast ...

- Talið af sérfræðingum, verðfall á ríkisskuldabréfum Bandaríkj...

Eldri færslur

2025

2024

2023

2022

2021

2020

2019

2018

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

Nýjustu myndir

Bloggvinir

-

eyglohardar

eyglohardar

-

bjornbjarnason

bjornbjarnason

-

ekg

ekg

-

bjarnihardar

bjarnihardar

-

helgasigrun

helgasigrun

-

hlini

hlini

-

neytendatalsmadur

neytendatalsmadur

-

bogason

bogason

-

hallasigny

hallasigny

-

ludvikjuliusson

ludvikjuliusson

-

gvald

gvald

-

thorsteinnhelgi

thorsteinnhelgi

-

thorgud

thorgud

-

smalinn

smalinn

-

addabogga

addabogga

-

agnarbragi

agnarbragi

-

annabjorghjartardottir

annabjorghjartardottir

-

annamargretb

annamargretb

-

arnarholm

arnarholm

-

arnorbld

arnorbld

-

axelthor

axelthor

-

arnith2

arnith2

-

thjodarsalin

thjodarsalin

-

formosus

formosus

-

birgitta

birgitta

-

bjarnijonsson

bjarnijonsson

-

bjarnimax

bjarnimax

-

westurfari

westurfari

-

virtualdori

virtualdori

-

bookiceland

bookiceland

-

gattin

gattin

-

davpal

davpal

-

dingli

dingli

-

doggpals

doggpals

-

egill

egill

-

jari

jari

-

einarborgari

einarborgari

-

einarsmaeli

einarsmaeli

-

erlaei

erlaei

-

ea

ea

-

fannarh

fannarh

-

fhg

fhg

-

lillo

lillo

-

gesturgudjonsson

gesturgudjonsson

-

gillimann

gillimann

-

bofs

bofs

-

mummij

mummij

-

gp

gp

-

gudmbjo

gudmbjo

-

hreinn23

hreinn23

-

gudrunmagnea

gudrunmagnea

-

gmaria

gmaria

-

topplistinn

topplistinn

-

skulablogg

skulablogg

-

gustafskulason

gustafskulason

-

hallurmagg

hallurmagg

-

haddi9001

haddi9001

-

harhar33

harhar33

-

hl

hl

-

diva73

diva73

-

himmalingur

himmalingur

-

hjaltisig

hjaltisig

-

keli

keli

-

fun

fun

-

johanneliasson

johanneliasson

-

jonsullenberger

jonsullenberger

-

rabelai

rabelai

-

jonl

jonl

-

jonmagnusson

jonmagnusson

-

jonvalurjensson

jonvalurjensson

-

thjodarskutan

thjodarskutan

-

gudspekifelagid

gudspekifelagid

-

juliusbearsson

juliusbearsson

-

ksh

ksh

-

kristbjorg

kristbjorg

-

kristinnp

kristinnp

-

larahanna

larahanna

-

leifurbjorn

leifurbjorn

-

lifsrettur

lifsrettur

-

wonderwoman

wonderwoman

-

maggij

maggij

-

elvira

elvira

-

olafureliasson

olafureliasson

-

olinathorv

olinathorv

-

omarragnarsson

omarragnarsson

-

ottarfelix

ottarfelix

-

rafng

rafng

-

raksig

raksig

-

redlion

redlion

-

salvor

salvor

-

samstada-thjodar

samstada-thjodar

-

fullvalda

fullvalda

-

fullveldi

fullveldi

-

logos

logos

-

duddi9

duddi9

-

sigingi

sigingi

-

sjonsson

sjonsson

-

sigurjons

sigurjons

-

stjornlagathing

stjornlagathing

-

athena

athena

-

stefanbogi

stefanbogi

-

lehamzdr

lehamzdr

-

summi

summi

-

tibsen

tibsen

-

vala

vala

-

valdimarjohannesson

valdimarjohannesson

-

valgeirskagfjord

valgeirskagfjord

-

vest1

vest1

-

vignir-ari

vignir-ari

-

vilhjalmurarnason

vilhjalmurarnason

-

villidenni

villidenni

-

thjodarheidur

thjodarheidur

-

valli57

valli57

-

tbs

tbs

-

thorgunnl

thorgunnl

-

thorsaari

thorsaari

-

iceberg

iceberg

Heimsóknir

Flettingar

- Í dag (23.9.): 8

- Sl. sólarhring: 9

- Sl. viku: 412

- Frá upphafi: 871515

Annað

- Innlit í dag: 6

- Innlit sl. viku: 382

- Gestir í dag: 6

- IP-tölur í dag: 6

Uppfært á 3 mín. fresti.

Skýringar